Student Loan Payments Resume in 2026: The Financial Shock Coming Your Way (And How to Prepare)

New to personal finance and investing?

If you're just getting started, I recommend checking these out first:

- How to Start a Budget — the foundation of money management

- How to Build Wealth From Zero — the equation that explains wealth multiplication

- Financial Levels Step by Step — where debt payoff fits in your strategy

Your phone buzzes during lunch. It's your loan servicer confirming your new payment schedule.

For three years, you've been free. No federal student loan payments. The pandemic pause gave you breathing room to save, pay down debt, maybe start investing. It felt permanent—like the government had finally given regular people a break.

Then you see the number: $287 per month starting June 2026.

Your stomach drops. You do the math quickly: $287 × 12 months = $3,444 per year. That money was already earmarked. Credit card payoff. Emergency fund. Maybe a vacation. Now it's gone.

You are not alone. 42.8 million federal student loan borrowers are staring at the same shock right now. And here's what most people don't know: the actual cost is far worse than the monthly payment. There's a tax bomb coming. The SAVE plan is being eliminated. New rules are reshaping how forgiveness works. And your FIRE timeline might be in serious trouble.

This article walks you through every change happening in 2026, shows you the exact math of the shock, and gives you step-by-step strategies to navigate it without destroying your financial goals.

The Pause Ends: What Happens on Day 1 of Repayment

Let me start with what's actually happening and when.

The federal student loan payment pause—which started in March 2020 as pandemic relief—officially ended in October 2023. Technically, borrowers were supposed to resume payments then. But the government gave people a soft landing: no payments were actually due until June 2024. No interest accrued. No penalties. It was extra grace.

By June 2026, that grace period evaporates completely.

Starting June 1, 2026:

- Payments are due on their normal schedule

- Interest accrues daily (it already is, but the government stopped adding it during the pause)

- Default consequences restart (wage garnishment, tax refund seizure, credit damage)

- Collection activity intensifies

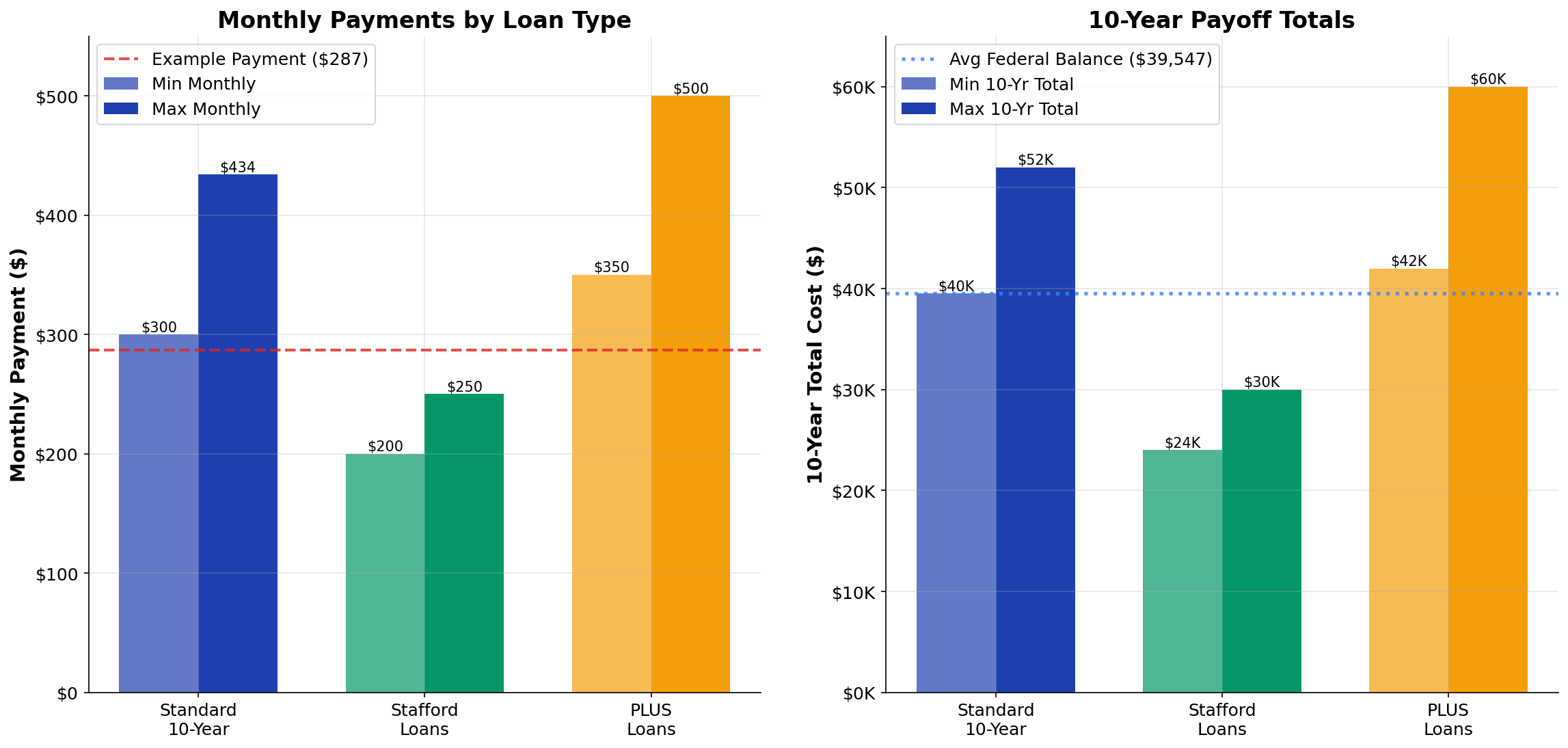

For a typical borrower with $39,547 in federal loans (the current average), here's what you're looking at:

| Loan Type | Average Monthly Payment | Interest Rate | 10-Year Payoff Total |

|---|---|---|---|

| Standard (10-year) | $300-$434 | 5-7% | $39,500-$52,000 |

| Stafford Loans | $200-$250 | ~5.5% | $24,000-$30,000 |

| PLUS Loans | $350-$500 | 6-8% | $42,000-$60,000 |

| Income-Driven Repayment | $150-$300 | Same | $40,000-$65,000 (with tax bomb) |

Here's the real shock: the government estimates that 12 million borrowers (or 1 in 4) will struggle to make these payments. Many will slip into delinquency. Some will default. And that means the machinery of default—wage garnishment, tax refund seizure, collection agencies—kicks back into gear.

The Tax Bomb You Didn't See Coming: Forgiveness Is Now Taxable

This is the change that catches people off-guard more than anything else.

For the last three years, student loan forgiveness under income-driven repayment plans was tax-free. It was a temporary exemption from the American Rescue Plan Act (ARPA). It made sense: if the government forgave your debt, you shouldn't be taxed on it as "income."

That exemption expired on December 31, 2025.

Starting January 1, 2026, any student loan forgiveness under income-driven repayment plans (REPAYE, PAYE, IBR, or the new Repayment Assistance Plan) is treated as taxable income.

Let me show you what this actually means in dollars.

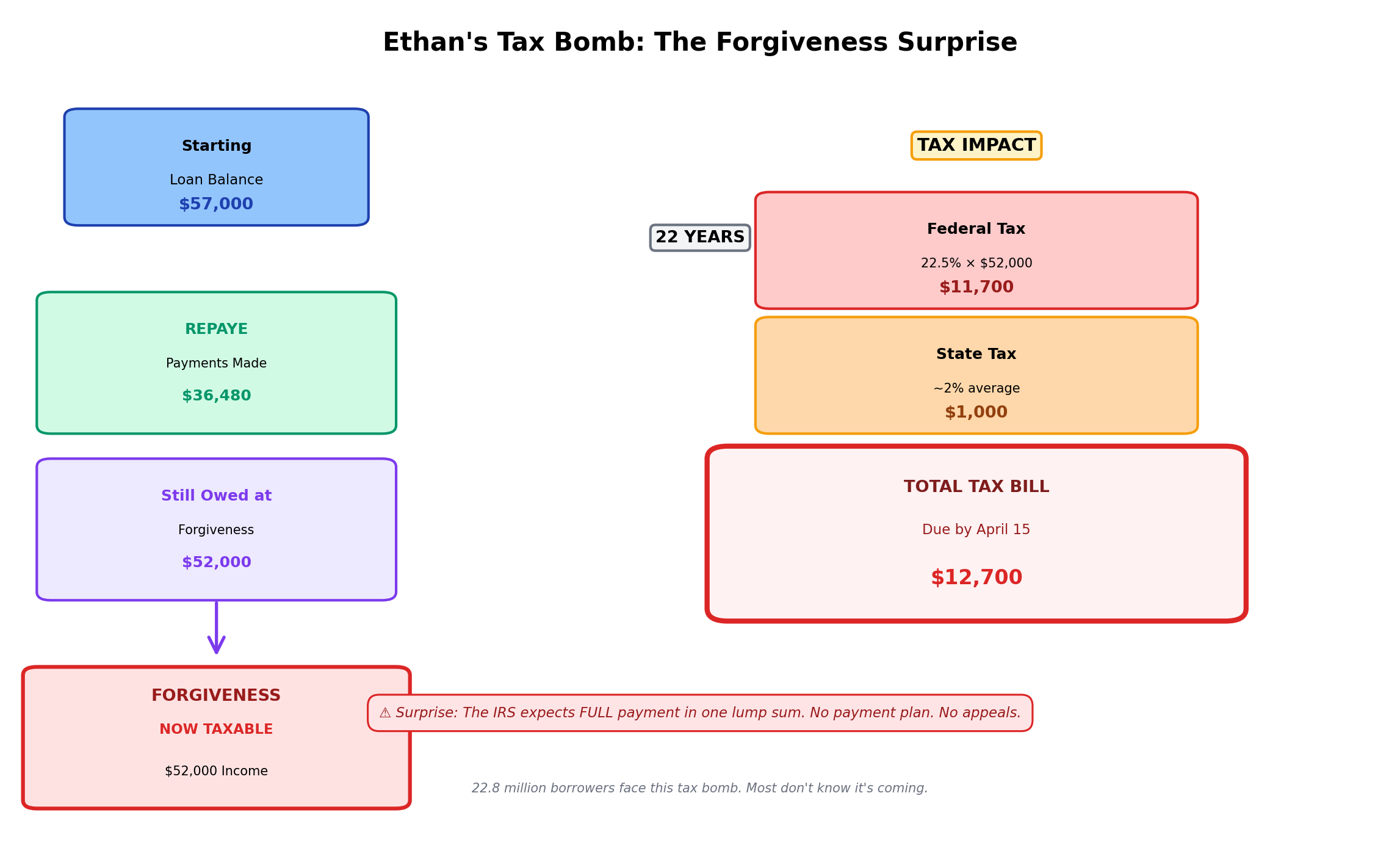

Meet Ethan. He's 42, earning $65,000 per year, and has $57,000 in federal student loans. He's been on REPAYE (income-driven repayment) for 8 years. His monthly payment has been around $380 based on his income. That's about $36,480 paid so far. He still owes $52,000.

If Ethan stays in REPAYE for 22 more years (age 64), the government forgives the remaining $52,000 balance.

Sounds great, right?

Wrong.

That $52,000 forgiveness is now reported to the IRS as taxable income. Depending on his tax bracket at age 64, he owes roughly $11,700 in federal taxes on the forgiveness (assuming a 22.5% marginal rate).

But there's more: that income bump might push him into a higher tax bracket. He might lose eligibility for certain credits. His state might tax it too—add another $500-1,500.

Total tax bill: $12,200-13,200.

And here's the cruelest part: the IRS will expect payment in full by the tax deadline. You don't get a payment plan. You don't get to spread it over years. You have one bill, due April 15th, with your tax return.

Now, here's who's not affected:

- Public Service Loan Forgiveness (PSLF) borrowers: your forgiveness is NOT taxable (this was specifically protected)

- Teacher Loan Forgiveness: NOT taxable

- Loans forgiven due to death or total permanent disability: NOT taxable

- Loans forgiven after borrower insolvency (rare): NOT taxable

But if you're on standard income-driven repayment? You're exposed.

The National Association of Student Financial Aid Administrators (NASFAA) estimates that the vast majority of borrowers in IDR plans are completely unaware their forgiveness will be taxable. They're planning to eventually hit the forgiveness point and assume tax-free money. They're wrong.

The SAVE Plan Is Dead: What Replaces It (Repayment Assistance Plan, July 2026)

Here's where the situation gets chaotic.

The SAVE plan (Saving on a Valuable Education)—which 7+ million borrowers are currently enrolled in—is being eliminated by court order, effective September 30, 2026. The plan was controversial because it allowed some borrowers with undergraduate loans to pay as little as $0/month (though interest still accrued).

Conservatives challenged it legally. They won. The plan is being killed.

Effective July 1, 2026, a new Repayment Assistance Plan launches, replacing it.

Here's what changes:

| Feature | SAVE Plan (Pre-2026) | Repayment Assistance Plan (July 2026+) |

|---|---|---|

| Undergraduate payment % of income | 5% of discretionary income | 5% of discretionary income (same) |

| Graduate loan payment % | 10% of discretionary income | 10% of discretionary income (same) |

| $0 payment eligibility | Yes (if income is low enough) | Eliminated—minimum interest-only payment |

| Forgiveness timeline | 20 years (undergrad), 25 (grad) | 20-25 years (same) |

| Tax bomb on forgiveness | Temporarily exempt through 2025 | Now taxable (see section above) |

The big hit: borrowers currently paying $0 on SAVE will move to interest-only payments starting July 2026.

If you're a borrower with $30,000 in loans at 5.5% interest paying $0 monthly on SAVE, your new RAP payment will be roughly $138/month (just covering interest). That's a jump from $0 to $1,656 per year.

For SAVE borrowers, this is a significant shock. You have until September 30, 2026 to stay on SAVE. After that date, the government will automatically move you to RAP. Or you can switch earlier to other plans (Standard, Extended, or alternative income-driven plans).

The good news: RAP maintains the 5-10% income-based calculation, so if your income is genuinely low, your payment stays manageable. The bad news: no more free ride on $0 payments.

Will They Take Your Tax Refund? 2026 Collection Rules Explained

This is real and happening now.

The Treasury Offset Program (TOP) allows the government to seize tax refunds from borrowers in default on federal student loans. This is a powerful collection tool—and it was paused during the pandemic relief period.

As of early 2026, the government is preparing to resume tax refund seizure for defaulted loans.

Here's who's at risk:

You're vulnerable if:

- You're 270+ days late on a federal student loan (roughly 9+ months)

- You're in default (not just delinquent—you've stopped paying entirely)

- You have a tax refund coming

Here's what happens:

You file your 2025 tax return expecting a $2,000 refund. The IRS cross-references your Social Security number with the Department of Education's default database. They find that you owe $18,000 in defaulted student loans.

Your $2,000 refund is seized and sent to debt collection.

You get a letter 30 days later explaining what happened. You're now $2,000 less for taxes, plus collection fees and penalties are added to your loan balance, making it even harder to climb out.

Now here's the tricky part: you also lose access to tax credits that should protect you.

The Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) are partially protected—but only partially. The government seized a portion of the EITC refund to offset student loan debt in 2025, affecting 365,000 households.

If you're in default or approaching delinquency, your move is to act now:

- Contact your loan servicer and ask about rehabilitation

- Rehabilitation requires 9-12 on-time payments, then your default status is removed

- Once rehabilitated, you regain refund protection

- Set up income-driven repayment to keep future payments manageable

The Treasury Offset Program was supposed to pause through early July 2026, but that deadline is fluid. Don't assume it won't happen. Act now if you're behind.

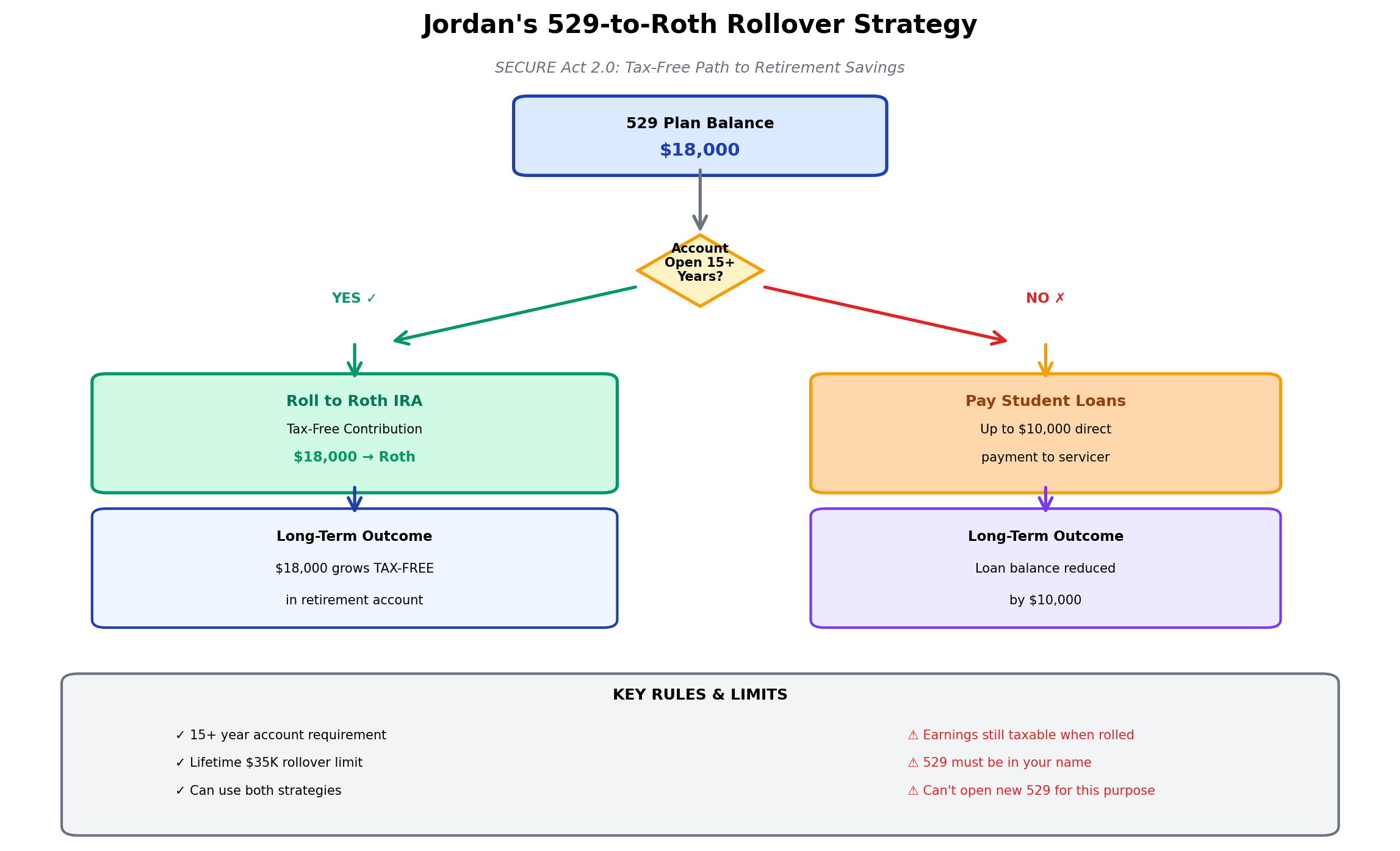

The 529-to-Roth Strategy: New 2026 Loophole for Student Loan Borrowers

Here's something that could actually help in 2026: the new 529-to-Roth rollover rules.

The SECURE Act 2.0 (passed in 2022, fully effective in 2026) created a new pathway: unused 529 education savings can roll into Roth IRAs.

Here's the math that makes sense for student loan borrowers:

Scenario: Jordan's Situation

Jordan is 28 with $35,000 in student loans. Her parents opened a 529 plan for college but she graduated with scholarships. The plan has $18,000 sitting unused.

Under the new rules, Jordan can roll up to $35,000 (lifetime) from 529 plans into her Roth IRA. The $18,000 rolls tax-free into the Roth. She now has $18,000 saved for retirement—money that was going to languish in a 529.

Additionally: the new SECURE Act allows up to $35,000 from 529s to pay off student loan debt directly. So if a parent has a 529, they can send $10,000 straight to Jordan's loan servicer to reduce her balance.

This isn't a silver bullet (most families don't have $35,000 in unused 529s), but if you have one—or your parents do—this is worth exploring.

Constraints:

- The 529 must have been open for 15+ years

- The contribution period is limited (you can't suddenly open a 529 and roll it into a Roth)

- Earnings on the 529 are still taxable when rolled

But for borrowers who have access, it's legitimate relief.

Student Loans vs. Investing: The FIRE Math in 2026

This is the decision that matters most for your long-term wealth.

Do you aggressively pay off loans, or do you invest the extra cash?

The answer depends on three variables: interest rate, psychological wins, and tax deduction limits.

The Math

Federal student loan interest rates are currently 5-7.5% depending on the loan type. The standard 10-year payoff is mathematically certain—pay X dollars, debt goes away.

Investing in a diversified portfolio historically returns 7-10% per year (average over 20+ years). But there's no guarantee. You could have a down year. You could have a decade that underperforms. If you're new to investing, Investing Made Simple breaks down why starting early matters even when loan payoff seems urgent.

The math seems to favor investing (higher expected return than loan interest rate). But here's where psychology and constraints come in.

The Tax Deduction Trap

You can deduct up to $2,500 per year in student loan interest. That's the limit. Period. If you're paying $8,000/year in interest, only $2,500 is deductible. The other $5,500 is sunk cost.

Compare this to mortgage interest (fully deductible for most homeowners) or tax-advantaged retirement accounts (pre-tax contributions). Student loans get minimal tax relief. For a deeper analysis of how different debt types compete for your money, see our breakdown of credit card interest rate traps and the math that keeps borrowers trapped.

This changes the calculus. If you're paying $8,000/year in interest and only $2,500 is deductible, your effective loan interest rate is closer to 7.5% instead of 5% (accounting for the tax benefit).

The Psychological Win

Here's what nobody mentions: paying off debt creates a psychological momentum that accelerates wealth-building.

Research shows that people who eliminate debt first (even if investing mathematically makes more sense) are more likely to maintain their savings rate long-term. Debt psychologically drains willpower. Eliminating it creates space to invest.

For people in FIRE communities, this matters. The fastest path to financial independence isn't always the one with the highest mathematical return. It's the one you'll actually stick with.

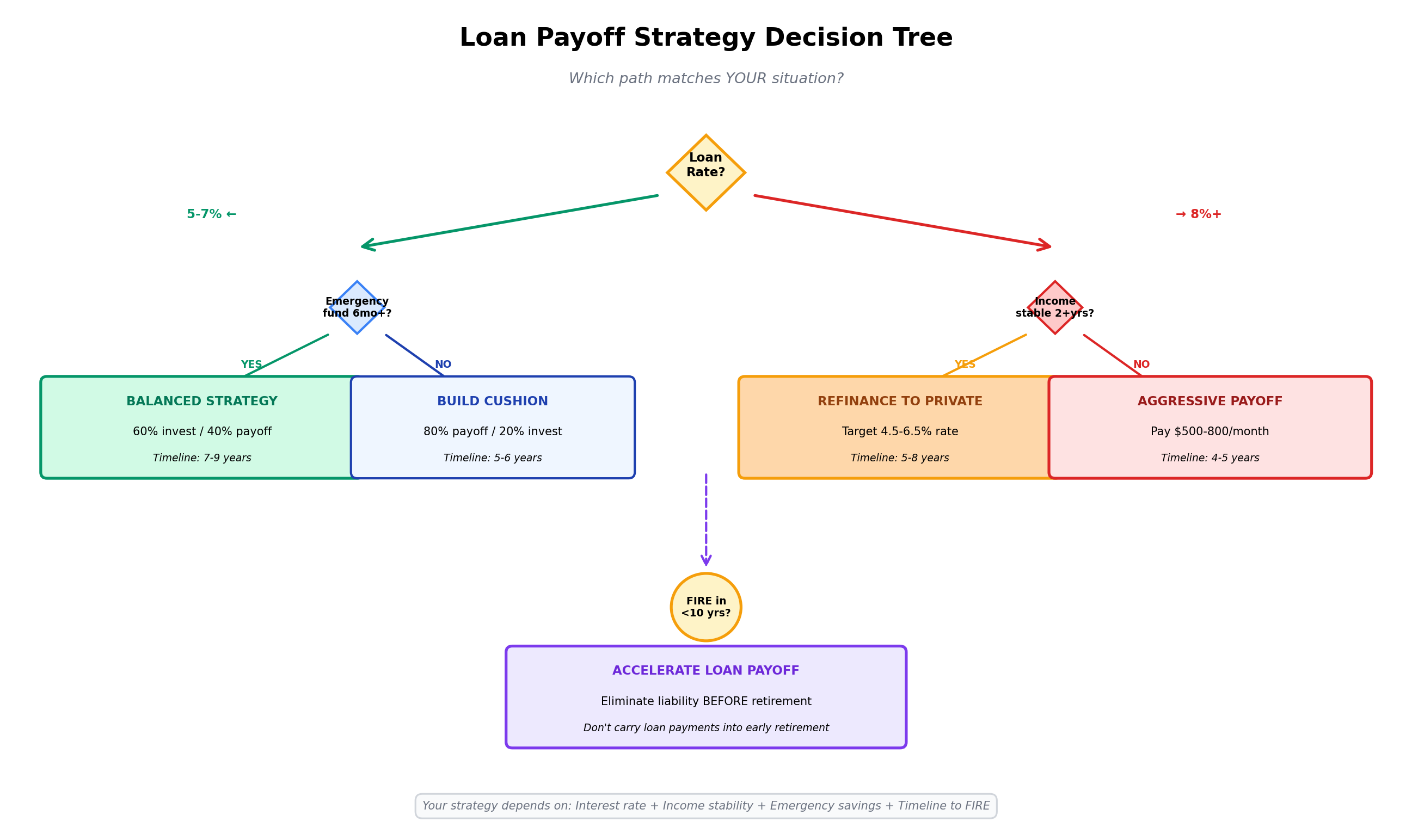

The Recommendation (By Situation)

Federal loans at 5-7% + stable income + already have 6-month emergency fund: → Invest 60%, aggressively pay loans 40%. You benefit from both.

Private loans at 8%+ + variable income + unstable employment: → Aggressively pay loans, minimal investing. Interest rate and income uncertainty favor debt elimination.

Income-driven repayment plan + expecting forgiveness + aware of tax bomb: → Calculate your expected tax bill 20-25 years out. Set aside funds for it monthly. Invest the rest. Don't get blindsided.

Early FIRE timeline (planning to retire in 10 years): → Accelerate loan payoff to eliminate the liability before retirement. You don't want loan payments eating your withdrawal budget in early retirement.

The Monthly Cash Flow: Budgeting for Payments + Protecting Your Savings Rate

Let me be direct about the shock: for millions of Americans, that $200-$434 monthly payment represents a 15-25% reduction in discretionary income.

If you're a single earner making $50,000/year after taxes ($3,300/month), a $300 student loan payment is 9% of your take-home. Add rent (30%), food (12%), utilities (6%), and you're at 57% of income allocated. Your savings rate just dropped.

How do you absorb this without gutting your financial goals?

The Budget Reallocation Strategy

Step 1: Audit the "pause money"

For three years, borrowers directed loan payment money to emergency funds, credit card payoff, or investments. Track exactly where that cash went. If $300/month was going to a credit card, $200 was going to savings, and $100 was discretionary, your payoff should rebalance these proportions—not eliminate all three.

Step 2: Reduce the categories that will adjust fastest

Not all spending is equal. Some categories (rent, utilities) are fixed. Others (dining out, subscriptions, entertainment) are flexible. When you need to free up $300/month, target flexible categories first.

Average American subscriptions: Netflix, Hulu, Spotify, gym, meal kit, etc. = $150-200/month. Cut low-ROI subscriptions.

Dining out budget: average American spends $300+/month eating out. Cut to 50% using meal prep.

You've just freed up $200-250 in flexible cuts, bringing the shock from $300 to $50-100.

Step 3: Recover 1-3% from income or side income

A 5-10 hour/month micro side hustle (freelance work, tutoring, selling items) at $25/hour = $125-250/month. This covers the remaining gap without cutting into your savings rate.

The key insight: the goal isn't to maintain the exact same spending in all categories. It's to maintain your overall savings rate.

Your savings rate is sacred. If you're saving 15% of gross income, the goal is to stay at 15% — not to stay at the same discretionary lifestyle.

The Tools That Help

How to Start a Budget is essential here. You need visibility into where money is actually going, not where you think it's going.

Use MFFT's budget tool to tag expenses by priority. Set allocation limits by category. The forced visibility makes it dramatically easier to spot the $150/month in subscription waste or the $200/month in impulse purchases that can be redirected.

For borrowers serious about FIRE, protecting your savings rate during this shock is more important than which specific debt payoff strategy you choose.

Strategic Payoff Roadmap: 5-Year Payoff vs. Income-Driven vs. Strategic Default

Not all loan payoff strategies are created equal. Your choice here determines whether student loans accelerate or derail your financial goals.

Strategy 1: Aggressive 5-Year Payoff

How it works:

- Throw everything at loans beyond minimum payment

- Pay $500-800/month instead of $200-300/month

- Goal: Eliminate debt in 5 years instead of 10

Pros:

- You own the timeline (5 years vs. 20+ years)

- Minimal interest paid

- Huge psychological win

- Protects your FIRE timeline by removing liability

Cons:

- Requires $12,000-48,000 in cash flow over 5 years

- Opportunity cost: that money in S&P 500 would grow

- You're sacrificing present financial flexibility

- If income drops, you're unprepared

Who should do this:

- High earners ($75,000+) with stable jobs

- People planning FIRE within 10-15 years (loans become a liability)

- Anyone with private loans at 8%+ interest

Strategy 2: Income-Driven Repayment (20-25 Year Stretch)

How it works:

- Stay on REPAYE, PAYE, or RAP

- Pay 5-10% of discretionary income

- Government forgives remainder after 20-25 years

- But pay the tax bomb out of pocket

Pros:

- Minimum payment as low as $100-150/month

- Maximum flexibility if income drops

- Protects FIRE by freeing up cash for investments

- Simple: set payment, pay it, move on

Cons:

- Total cost is often higher due to interest accrual

- Forgiveness is taxable (expect $10,000-20,000 tax bill at the end)

- Psychological drain of 20+ years of payments

- Plan includes an ambush tax liability

Who should do this:

- Lower-income borrowers ($35,000-50,000)

- Parents supporting kids or elderly relatives

- Anyone whose income is unstable

- Borrowers on PSLF (public service) whose forgiveness is tax-free

The Tax Bomb Planning: If you choose this route, you must set aside money monthly for the tax bomb. Here's how:

Calculate expected forgiveness amount (loan balance × 1.03-1.05 annually for 20+ years due to interest accrual). That might be $80,000-120,000 in forgiveness.

Expected tax rate: 22-24% federal + 5-8% state = 27-32% total.

Your tax bomb: $21,600-38,400.

Set aside $70-125/month in a separate savings account specifically for this liability. When forgiveness hits, you pay the IRS from that account, not from emergency funds or credit cards.

Strategy 3: Refinance to Private Loans (For High Earners Only)

How it works:

- Transfer federal loans to private lender

- Get interest rate based on creditworthiness (typically 4.5-6.5%)

- Lower interest = faster payoff option

Pros:

- Potentially lower interest rate than federal average

- Tighter payoff timeline if combined with aggressive payments

- Removes income-driven repayment option (forces accountability)

Cons:

- Lose federal protections (income-driven repayment, PSLF, public service deferment)

- Private lenders can't adjust payments if you lose job

- No deferment or forbearance options

- If you're expecting forgiveness or relying on income-driven flexibility, this is a trap

Who should do this:

- High earners ($100,000+) with rock-solid job security

- Borrowers NOT planning to use income-driven repayment

- Anyone with federal rates above 6.5% and private offers below 5%

Who should NOT do this:

- Anyone with unstable income

- Anyone planning FIRE (you want flexibility)

- Borrowers expecting forgiveness

- Anyone not certain they'll stay employed in one field

Action Steps: What to Do Right Now (April 2026)

Stop reading and do these things this week.

Action 1: Know Your Loans (This Week)

Go to StudentAid.gov. Log into your account. Find:

- Exact balance on each loan

- Interest rate for each loan

- Current servicer information

- Current repayment plan

Write these down. You need this information to do the math.

Action 2: Calculate Your June 2026 Payment (This Week)

Based on your plan and balance, calculate your expected payment:

- Standard 10-year: use loan balance ÷ 120 months (rough estimate)

- Income-driven: use Federal Student Aid calculator at StudentAid.gov

- SAVE to RAP transition: note your current $0 payment will become interest-only (~0.5% monthly)

Action 3: Set Up Automatic Payments (Before June 1)

The government incentivizes automatic payments by giving you 0.25% interest rate reduction. More importantly, you won't miss a payment and accidentally default.

Set up autopay before June 1, 2026. Not in May. Not the week before. Now.

Action 4: Create a Payment Cushion (Next 30 Days)

Open a separate savings account called "Student Loan Payment Reserve" and deposit 3 months of expected payments into it. If your payment is $300/month, deposit $900.

Why? If you lose your job, have a medical emergency, or face an unexpected expense in June-August 2026, you won't be forced to default. You'll have a buffer.

Action 5: Choose Your Strategy (Next 30 Days)

Based on the frameworks above, decide:

- Aggressive 5-year payoff, or

- Income-driven stretch, or

- Refinance to private

Write it down. Share it with someone. Make it real.

If you choose income-driven repayment, set up monthly tax bomb savings immediately (see math above).

Action 6: Update Your Budget (This Month)

Use How to Start a Budget to recalculate your savings rate with the new loan payment included. Don't guess. Calculate it.

Protect your savings rate. That's the lever that builds wealth.

Action 7: Contact Your Servicer Before June 1

If you have questions about your servicer, contact them now. Don't wait until July when they're swamped.

Ask:

- "What is my exact payment amount starting June 2026?"

- "Can I set up automatic payments?"

- "If my income changes, can I switch repayment plans?"

- "Do I qualify for PSLF if I work in public service?"

One 10-minute phone call now prevents 6 months of confusion later.

The Bottom Line: Student Loans vs. Your FIRE Timeline

Here's what I want you to understand at the core level.

Student loans are not a moral failing. They're a financial obligation that needs a strategy.

For the millions of Americans in the FIRE community (or aspiring to be), student loan payments resuming in 2026 represents a critical inflection point. You can either:

- Fight the payments (aggressive payoff, clear your debt in 5 years, rebuild savings after)

- Manage the payments (income-driven repayment, minimum payments, invest the rest, plan for the tax bomb)

- Ignore the payments (default, face wage garnishment and credit destruction, spend the next decade recovering)

Option 3 is off the table. That path leads to financial catastrophe and makes FIRE impossible.

Between options 1 and 2, there's no universally "right" answer. It depends on your income stability, timeline, and risk tolerance.

But here's what's non-negotiable: you must choose and act on it by June 2026.

The government will resume collections. The tax bomb will come for income-driven repayment borrowers. The monthly payments will hit your cash flow. Ignoring it doesn't make it go away.

Emergency Fund 2026 explained why 59% of Americans can't cover a $1,000 emergency. Student loans resuming is exactly why that emergency fund is critical—it's your protection against the shock.

Building wealth from zero requires mastering the variables you control: income, spending, and time. Student loans are a spending category. Mastering them means deciding your strategy, calculating its cost, and executing it with discipline.

For FIRE, the movement towards early retirement has always been built on one principle: control your cash flow, maximize your savings rate, and let compound interest do the work. Student loans are a cash flow challenge. But they're not insurmountable.

You have the tools. You have the information. You need the action.

Pick your strategy this week. Set up your payment mechanism by May 1. Absorb the shock into your budget by June 1.

Your future self will thank you for getting ahead of this.

Ready to Protect Your Financial Goals?

Student loans are one lever in your wealth equation. But they're not the only one.

Use MFFT's budget tool to model how loan payments affect your overall financial plan. See your savings rate. Track your net worth. Plan for the tax bomb.

If you're serious about FIRE, understanding your loan strategy isn't optional—it's foundational.

What's your move for June 2026? Let's build the plan.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyChatGPT Just Got Your Bank Account: What OpenAI's Personal Finance Launch Means for Your Money (And Why a Dedicated Tool Still Wins)

On May 15, 2026, ChatGPT Pro linked to your bank via Plaid. Here is what it actually does, the 4 privacy red flags, and why a dedicated tool still wins.

Master Your Money

Master Your MoneySequence of Returns Risk in 2026: Why Retiring Into This Market Could Cost You 27 Years (And the Playbook to Avoid It)

Two retirees, same $1M, same 6.5% average return — one ends with $3.2M, the other is broke at year 27. That's sequence of returns risk in one chart, and 2026's CAPE 40 + 3.8% CPI setup makes it the most dangerous decade in 20 years. The 5-layer playbook to defuse it.

Master Your Money

Master Your MoneyYour Employer Just Killed the 401(k) Match to Pay for AI: The 2026 Survival Plan When Free Money Disappears

TTEC just suspended its 401(k) match for 16,000 employees to fund AI. Sherwin-Williams, Deloitte, and Zoom did similar in 2025-26. Here's the dollar damage by salary band, why this is happening, and a 6-step survival playbook to claw back the lost compounding.

Master Your Money

Master Your MoneyThe CD Ladder Comeback: How to Lock In 2026 Yields Before the Fed Cuts Rates Again

High-yield savings rates are dropping with every Fed cut in 2026, and most savers are losing yield without realizing it. A CD ladder freezes today's rates on most of your cash while keeping a chunk accessible each year. Here's the exact math, three ladder designs, and the three mistakes that turn a smart move into a mousetrap.

Master Your Money

Master Your Money401(k) Hardship Withdrawals Hit Record 6%: Why Americans Are Raiding Retirement (And the Real Cost)

401(k) hardship withdrawals hit 6% in 2025 — triple pre-pandemic. The real cost, 7 better alternatives, and the buffer keeping retirement untouchable.